Post

by Will Williams » Mon Jul 14, 2025 9:04 pm

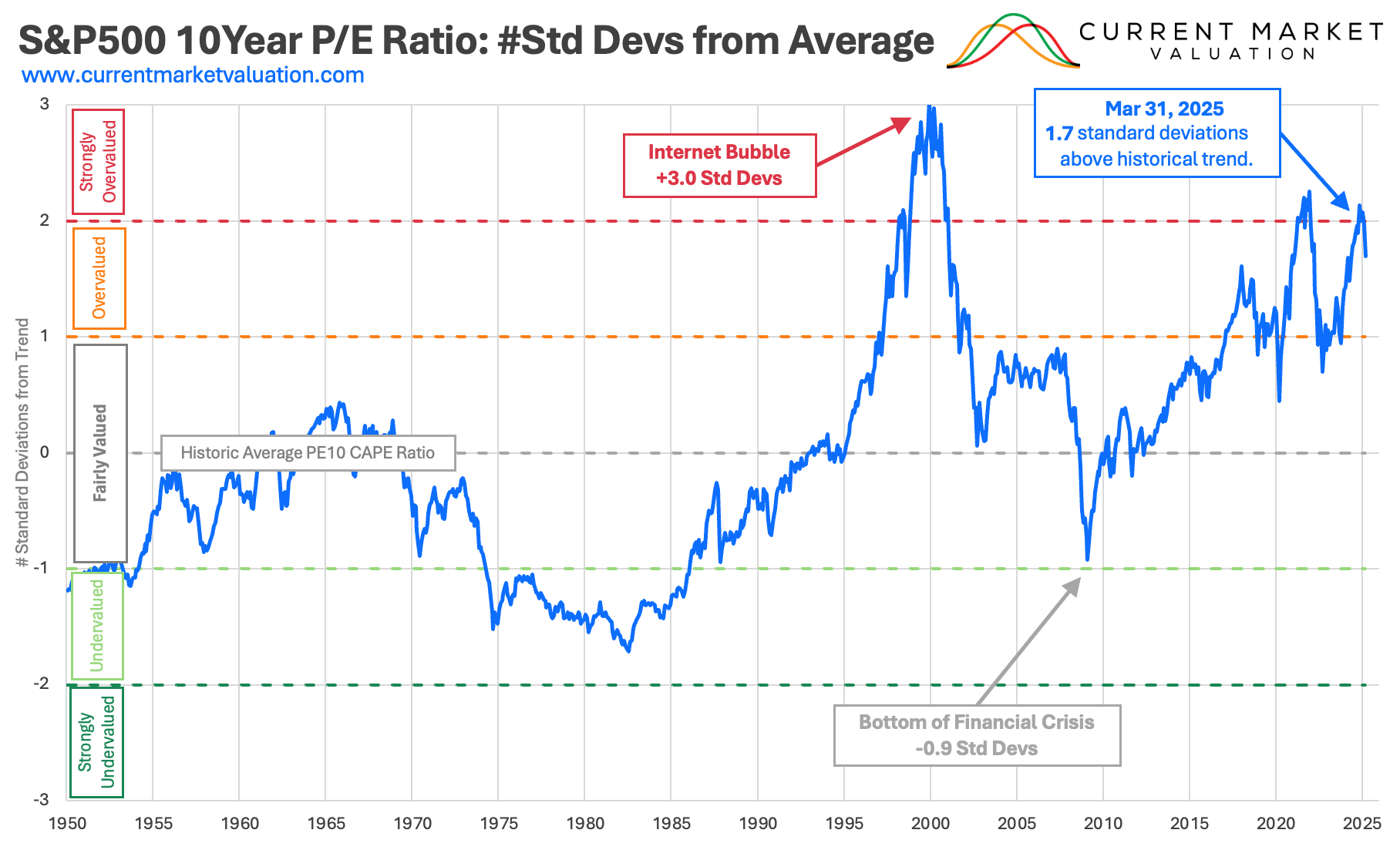

Yes, the Stock Market is setting new records now, but the bubble could burst at any time. Folks are speculating, gambling to invest in Wall Street. It may be better than buying lottery tickets or gambling in Vegas where "the house always wins." A better investment is in land, or better still, in the National Alliance.

I received this report today. It assumes the US will still be around years from now, but things are not looking that rosey. Economics is not called the "dismal science" for nothing. Some details here, though, about the US national debt and how the country got there:

Precious Metals News

July 14, 2025

How will rising national debt affect your finances?

From Elizabeth Djinis in 7/11 Yahoofinance.com

“On July 4, President Trump signed his “big, beautiful” domestic policy bill, enacting a new wave of tax cuts estimated to add $3 trillion to $4 trillion to the national debt.

While the national debt may be hard to conceptualize, economists say its explosive growth has the potential to have major impacts on the economy that will be felt even by individuals.

“I liken it to a boa constrictor squeezing its prey — the debt is slowly doing the same to the American economy,” said Brett Loper, executive vice president of policy at the Peter G. Peterson Foundation, which commissioned a number of recent reports on the national debt. “The squeeze comes in the form of slower growth, less job creation, higher costs of borrowing for consumers buying homes, or businesses investing in equipment. All of these are consequences.”

Apart from the tax legislation’s predicted impact, the total debt has nearly tripled in the last 20 years, from $12.26 trillion in 2004 to $35.46 trillion in 2024, per data from the U.S. Treasury. A slow and steady rise began in the 1980s and was accelerated by the 2008 financial crisis and Great Recession after a period of relative stagnation post-World War II. At the same time, the debt-to-GDP ratio, comparing the size of the debt to the U.S. gross domestic product, has continued to grow, first reaching 100% in 2013 and up to 123% last year. The ratio had not ticked above 100% since right after World War II.

The total amount the U.S. government is spending on interest has also continued to make up a bigger percentage of overall expenditures, from 8% in fiscal year 2019 to 13% in FY 2024, per numbers from the U.S. Government Accountability Office. In 2024, net interest was the third-largest federal spending category, at $881.7 billion, after Social Security and other federal healthcare.

How did we get here, and what drives the national debt?

To put it in simple terms, the U.S. national debt is the difference between the amount of money the federal government is bringing in through taxes and other revenue versus the total amount of budgeted federal spending, in addition to deficits from previous years, said Steven Kyle, associate professor of applied economics and management at Cornell University.

Part of the increase in recent years is attributable to the COVID-19 pandemic, which ushered in a variety of special spending, as well as the regular drivers, including entitlement programs like Medicaid and Medicare, defense spending, and high interest on the debt itself, said University of Pennsylvania Wharton School professor of finance Itamar Drechsler. Increasing costs to maintain Medicare and Social Security, due to an aging population and the rising price of healthcare, have also helped drive up the national debt.

While much has been made about the debt-to-GDP ratio in recent years, Kyle notes that there’s no exact percentage that indicates instability. Japan’s ratio, for example, was at almost 250% in 2023, yet that nation is not considered to be in an insecure economic position.

“There is no magic level for that number that means a crisis,” Kyle said. “… The problem we’re having right now is that people are doubting that the economic managers of the United States are serious people and that they’re actually trying to address this.”

What is clear, according to Kyle, is that one way to address an increase in government spending would be a boost in revenue through higher taxes. But in this current political atmosphere, that almost certainly won’t happen.

“On the revenue side, one where you are not allowed to utter the word tax, we have not been getting the revenue we need to cover the gap,” Kyle said. “And, therefore, we’ve been accumulating national debt in good times and bad.”

While what Kyle calls the “huge borrowing spree” of the pandemic was largely “unavoidable,” the last few years could have been used to right the financial ship.

The national debt is projected to top $52 trillion by 2035, according to the Congressional Budget Office — an estimate reached before Trump’s tax cuts were enacted.

How could ballooning national debt can affect your personal finances

Using a 2055 scenario in which the debt-to-GDP ratio is at 156%, the Peterson Foundation published an analysis which found that the current path of debt could reduce the size of the economy by $340 billion in 2035, shrink the number of U.S. jobs by 1.2 million, and bring wages down by 0.6% relative to having an unchanged national debt.

A 2025 Yale Budget Lab report showed that a permanent deficit increase of 1% of GDP would lead, after five years, to consumers paying $60 more in annual auto loan interest, $600 more in annual mortgage interest, and about $1,000 more for small business loan interest. The general tone of a continually rising national debt and debt-to-GDP ratio is some level of doom.

“What happens when everybody gets nervous?” Kyle said. “Consumers don’t buy things, investors don’t invest in new productivity capacity because they don’t know what their profit margin is going to be next year. We get a recession, and that can affect people.”

Depressed wages and jobs

According to the Peterson analysis, the number of U.S. jobs could decrease by as much as 1.2 million in 2035 and 2.7 million in 2055 based on the projected trajectory of the national debt compared to if it were to stay at its current level.

This could also lead to a decrease in wages as high as 3% by 2055. Essentially, a rising federal debt means the opposite of wage growth.

Higher taxes

One of the simplest ways to reduce the national debt is by increasing government revenue, and that is largely done through higher tax rates.

“Unless we have miraculous growth, that tax rate will have to rise on people,” Drechsler said. “… But it’s becoming increasingly toxic to ever talk about raising them, so in this political climate, I’m not sure it’s going to happen anytime soon.”

Higher interest rates

Whenever economists talk about economic growth, or a lack thereof, interest rates are generally the metric that follows. Higher interest rates determine who can buy property and cars and invest in a business.

“If [government debt] gets bigger and bigger, interest rates are going to be going up, because deficits are a direct stimulus to the economy. If they run huge budget deficits, then the Federal Reserve will raise interest rates to keep inflation in check,” Kyle said. “There’s only a certain amount of money looking for a home to be invested in and if the federal government soaks up ever more of it, consumers will feel that.”

The Yale Budget Lab found that after 30 years with a 1%-of-GDP permanent increase in the federal deficit, annual car loan interest would increase by $200 and annual mortgage interest on the median home by $2,300.

Inflation

Increased inflation is also a likely facet of a U.S. economy with an increasing national debt. The same Yale Budget Lab study noted that a deficit increase of 1% of GDP would raise inflation to the degree that, after five years, a household would lose $300 to $1,250 in purchasing power in 2024 dollars.””

If Whites insist on participating in "social media," do so on ours, not (((theirs))). Like us on WhiteBiocentrism.com; follow us on NationalVanguard.org. ᛉ